2025 was meant to be the year the bull market finally stumbled.

Download PDF VersionNo major economy is in recession, inflation is still falling back from its spike in 2022-23 and central banks have been cutting interest rates. The global economy has also displayed considerable resilience by shrugging off everything that has hit it in recent years. President Trump’s tariffs are the latest dog that didn’t bark and have not derailed the fundamentally benign economic backdrop. Moreover, corporate profits growth is very strong.

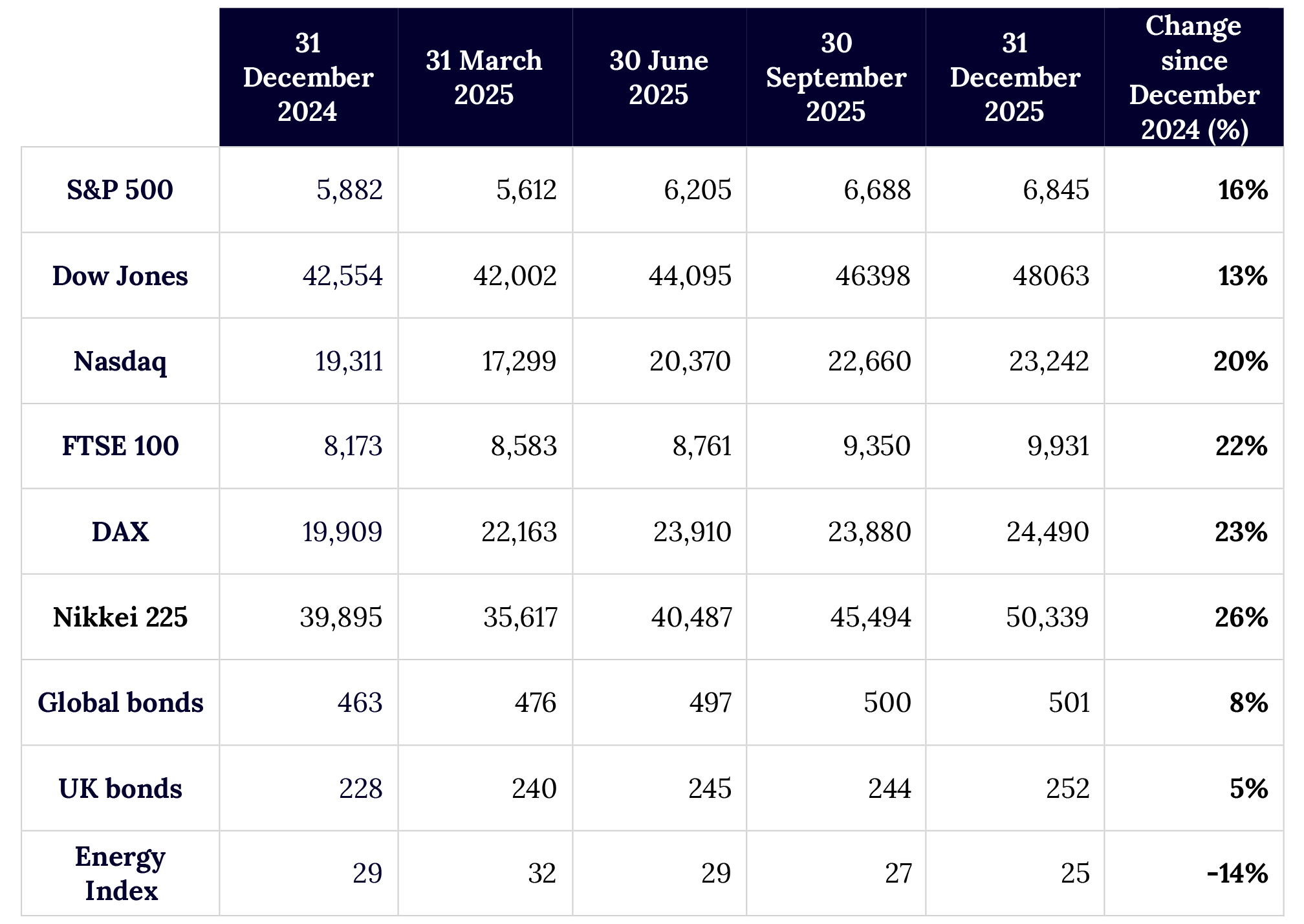

Defying fears about Donald Trump, sluggish economies, and an AI bubble, 2025 proved to be another strong year for stock markets (along with gold and other metals). US technology stocks were not the only game in town. Stock markets in Europe, Japan and many emerging markets outperformed the US in local currency and by even more once the weaker dollar was factored in.

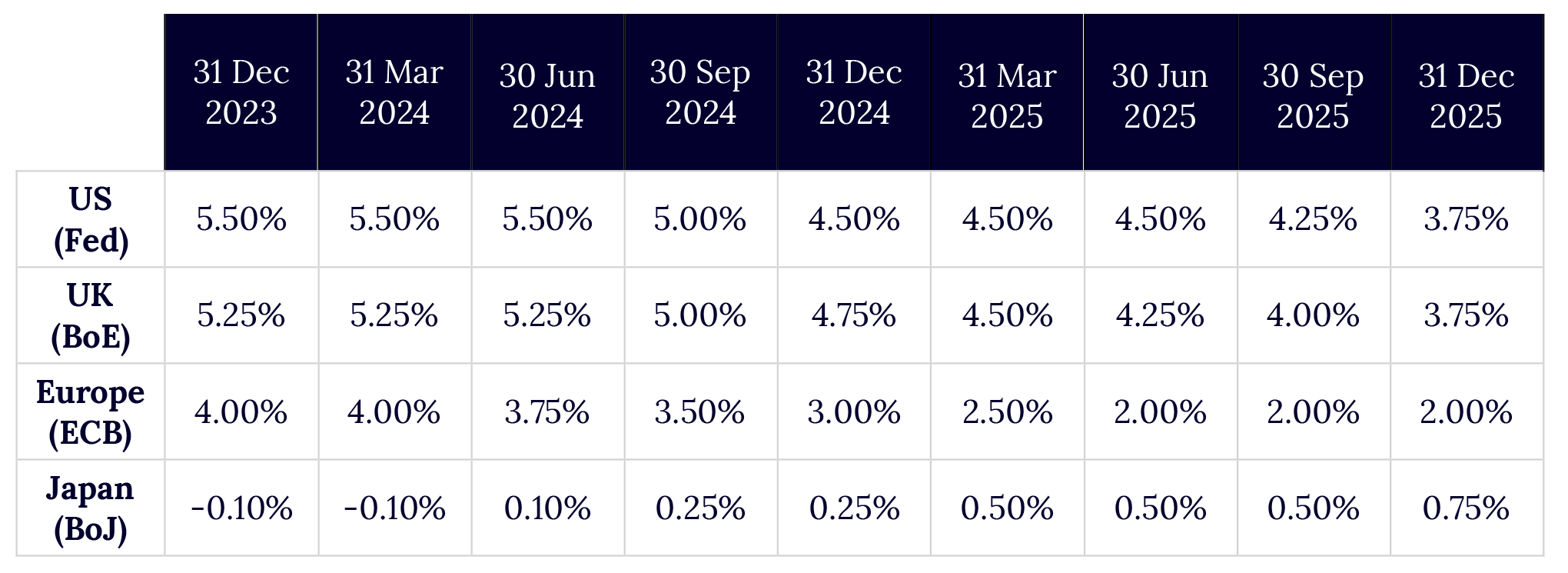

Last quarter, we shifted our market outlook from "cautiously optimistic" to “neutral” on the basis that the optimistic and pessimistic scenarios are now evenly balanced, and are sticking to this view. The most likely scenario for 2026 is more of the same: benign economies, falling inflation and gradual interest rate cuts. The benign state of the global economy has been a critical and underestimated driver of the equity bull market. But there are important risks. Probably the biggest economic risk is a possible pick-up in US inflation, which would throw a spanner in the works by stopping Fed rate cuts and raising long-term bond yields. Another common refrain is that we are in an AI bubble. While we do not believe we are in a bubble, this does not preclude a downturn in technology stocks or the AI story. An upset in another corner of the markets or a geopolitical event are, of course, also possible.

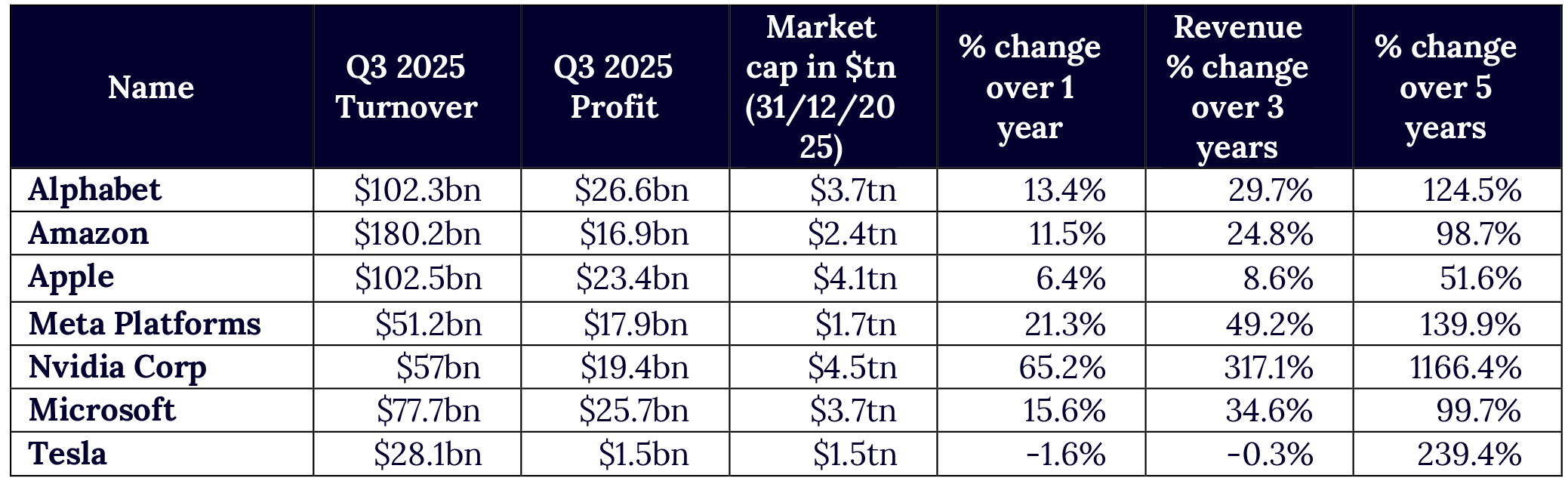

These days there is much talk of an AI bubble and no shortage of experts warning that the current equity bull market is destined to end in much the same way as the dotcom bubble of 1999-2000. It is certainly true that the Nasdaq index has risen inexorably in recent years, doubling since 2023. But this is relatively slow compared to the dotcom boom, when the index doubled in just six months between October 1999 and March 2000.

Perhaps the most important difference between then and now is that today’s leading technology companies are all hugely profitable and, in some cases, quasi-monopolies.

Our conclusion is that we are not in an AI bubble and do not face a re-run of the dotcom crash. Which is not to say, of course, that there will not be a correction at some point in technology stocks, either because AI adoption is slower than expected or for other reasons. By their nature such corrections are not pre-announced and are often fast and severe. But a peak-to-trough drawdown of almost 80% like we saw in 2000 to 2002 is highly unlikely in our view.

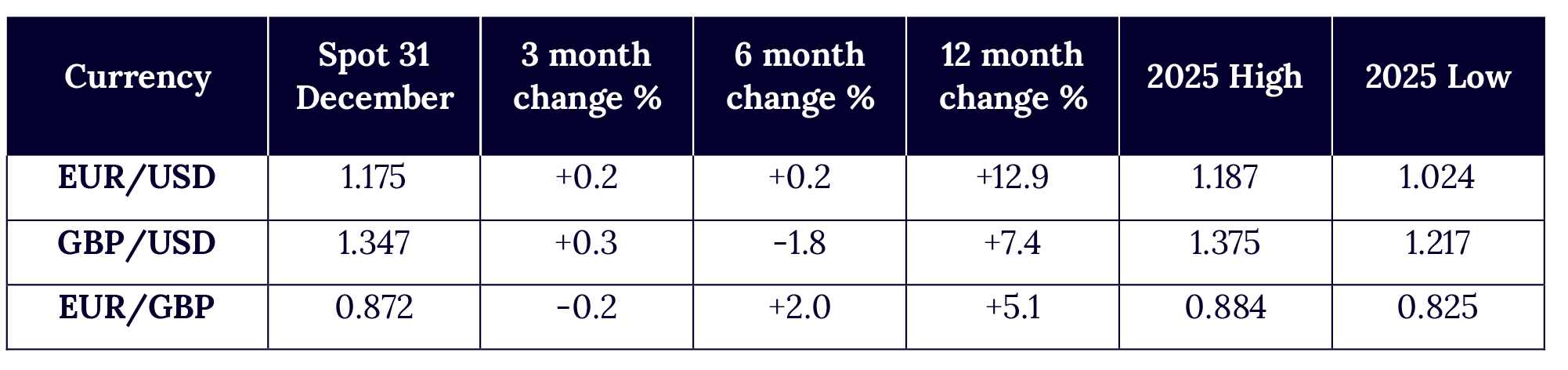

The following themes are intended as food for thought and do not represent a formal currency forecast.

Recent trend: neutral

Outlook: ambiguous

Recent trend: neutral

Outlook: neutral to up (weaker dollar)

Recent trend: neutral to down

Outlook: neutral to down (stronger sterling)

Our “neutral” outlook on the financial markets implies holding a moderate allocation in all mainstream asset classes. It would not be surprising if non-US and emerging stock markets outperform the US in 2026, just as they did last year. However, if there is a market downturn in 2026, ironically, US markets could outperform (and the dollar might also rise).

The way to deal with market downturns is to hold a well-diversified portfolio that cushions stock market losses and, in most cases, stay invested and await the upturn that inevitably follows in time.

One of the standout assets in 2025 was gold, which rose by a further 65% and is up over 100% over the last two years. As we have highlighted in past quarterly reports, the rally has been driven by a veritable cocktail of concerns, the most potent of which is possibly the weaponisation of the dollar, encouraging central banks to increase their holdings irrespective of price. While it is impossible to call the top for gold, we can be fairly certain that this year’s performance will not be repeated. Although gold remains a valuable hedge, there could be a case for lightening up on holdings or at least not adding at current levels.

Bonds are in some ways the linchpin asset class in 2026. If inflation continues to fall and central banks carry on cutting interest rates, bonds should perform well, but equities would probably remain the best-performing asset class. If, however, there is an inflation disappointment and central banks, particularly the US Federal Reserve, stop cutting interest rates, there could be a sell-off in the bond markets, which could potentially pull the rug from under the equity markets. In these circumstances, bonds would probably outperform equities. A downturn triggered by other risks, such as geopolitics or a market accident, would probably have similar effects.

Stock markets have had another good year. We are now neutral between optimistic and pessimistic views of the future, which implies pegging back risk a little. It is more important than ever to maintain a well-diversified portfolio, maintaining a moderate and geographically diversified exposure to all mainstream asset classes depending on each individual's situation. With our help, constant dialogue with your investment manager is the key to understanding your own risk/reward asset allocation.

Mark Estcourt

CEO