Oil prices have fallen back, the risk of military escalation has receded, and we have moved our outlook from cautious back to neutral.

Download PDF VersionPredictions of doom as a result of the Iran war were, once again, overdone. Even relatively moderate forecasts about the medium-term effects of the closure of the Hormuz Strait and the damage to energy production facilities were quickly rendered obsolete by the fall in the oil price. With the tail risk of a military escalation basically off the table, we are moving our outlook back from cautious to neutral. This means we expect the markets to be driven by macroeconomic and business fundamentals from here on.

As we have pointed out in all of our recent quarterly reports, it is easy to forget how positive the macroeconomic fundamentals are. The world economy is growing in sync, with no major region in recession, which in itself is relatively unusual. The pace of growth may not be that fast, but moderate growth is positive for corporate profits and helps to keep inflation contained.

In equity markets, the AI theme has become even more dominant, with individual stocks, industries and countries in many cases being divided into winners and losers based on their position in the AI infrastructure “stack”. Even if AI is not the only game in town – US small caps and value stocks have outperformed this year, for example – the importance of AI investment for growth in many economies, including the US, means that the macroeconomic outlook is now tied up with the fortunes of this technology, which creates a double dependency on this theme. Nonetheless, while a downturn or disappointment in the AI narrative would clearly be bad news for equity markets, it might not necessarily lead to a stock-market bust.

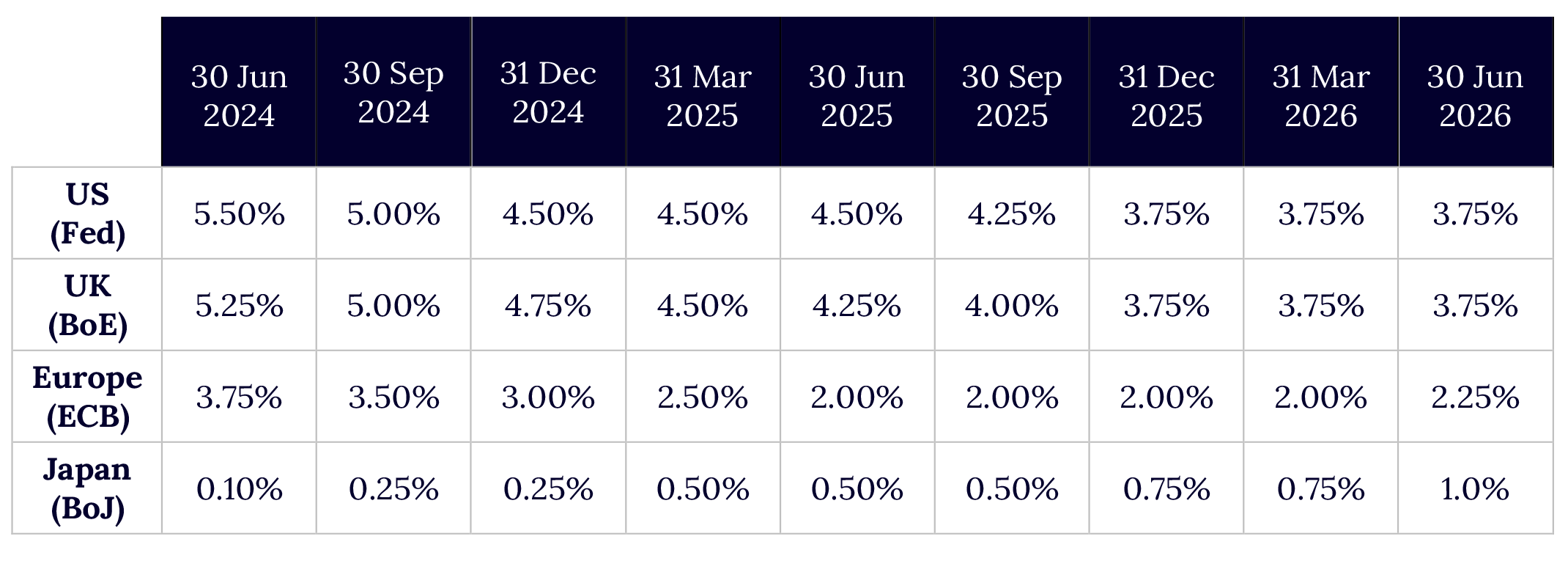

There are, therefore, still reasons for caution in the quarter ahead. A further risk, on top of concentration in AI stocks, is inflation and the risk of interest rate hikes, especially in the US. US core inflation has been sticky at an above-target level in recent quarters. It remains to be seen how severe and long-lasting any impact from higher oil prices proves to be. The new Fed chairman, Kevin Warsh, has warned that he is determined to deliver on the Fed’s inflation objective. While a rate hike or two might not be a disaster for the equity markets, they could clearly create a less favourable backdrop. A further risk is the ever-present geopolitical tensions erupting in several hotspots at any time.

Inflation developments in the US and other countries will be critical in setting the direction of monetary policy. The direction the US Fed takes will be key and a rate hike has the potential to cause market volatility. The strength of the US economy will also be an important input into the Fed’s thinking, with some recent data suggesting the labour market has rebounded this year.

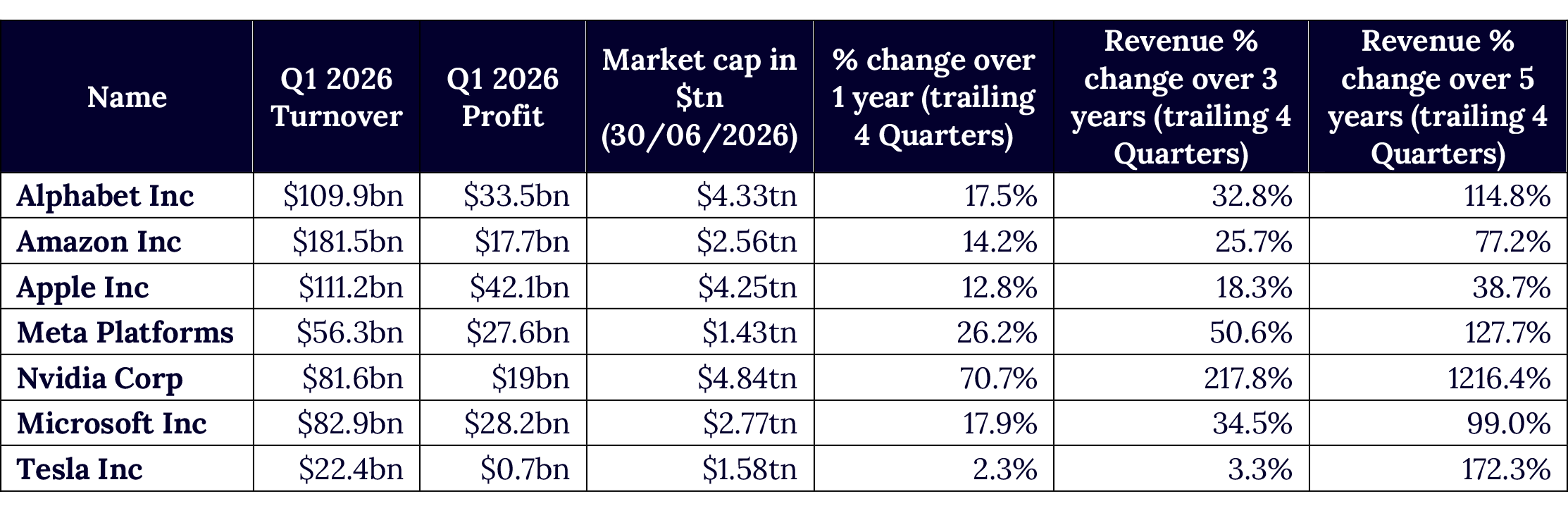

A new dimension will be added to the AI theme over the next six to nine months with the expected Initial Public Offerings (IPOs) of Anthropic and OpenAI. These will give the market access to pure play AI “labs” (model builders) for the first time. The IPOs will no doubt attract very high demand. This influx of capital has the potential to increase market concentration in the AI theme, which could distort markets. More incoming information on the revenues the hyperscalers, such as Microsoft, Meta, Amazon and Alphabet, are earning on their AI investments will also affect the narrative about the AI boom.

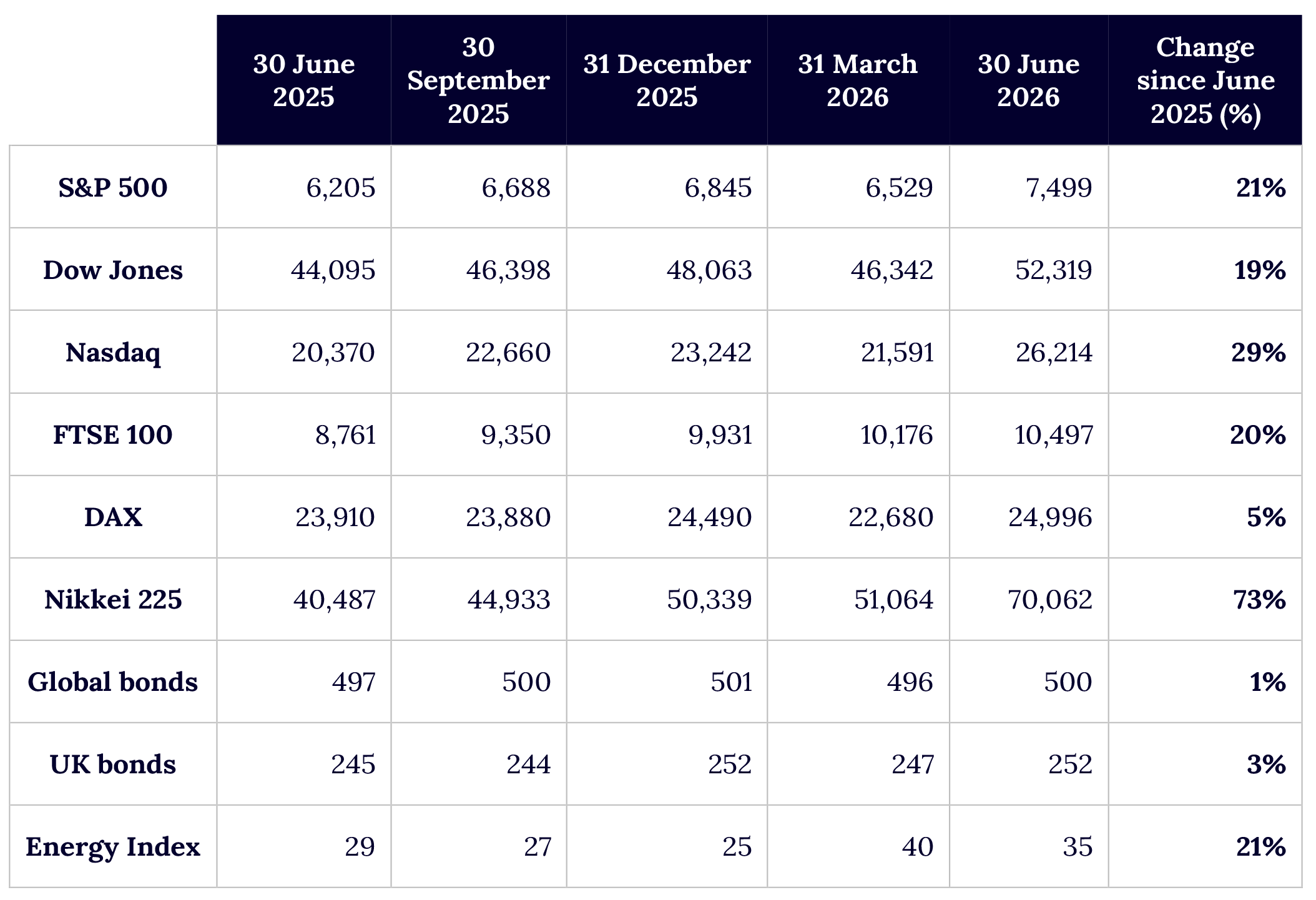

After a dip in the first quarter, technology stocks stormed back between April and June. The Nasdaq rose by over 20%. However, the index peaked in early June and was volatile in the final month of the quarter, as jitters about AI grew. Leadership has moved away from the Magnificent 7 (“Mag 7”), all of which, except Alphabet, underperformed over the quarter again, leading them to be rechristened the “Lag 7” by some analysts. The market has become concerned about the huge capital spending by the hyperscalers Meta, Microsoft, Alphabet and Amazon, which is eating up most of their free cash flow, and the lack of visibility on the returns on this investment. Heavy corporate users of AI are reported to be restricting use of the technology by staff in response to rising bills, casting doubt on some of the more optimistic revenue forecasts. Moreover, opposition to the construction of new data centres has become increasingly vocal and could upset the hyperscalers’ investment plans. The rising cost of memory chips is also squeezing margins. Microsoft and Meta have been the hardest hit and are down around 25% over the past year.

The immediate beneficiaries of the AI build-out have been chip manufacturers and their share prices have gone stratospheric this year. The Philadelphia Semiconductor Index in the US doubled in the first half of the year, with some individual stocks rising up to 3 to 8 times. It has been a similar picture for chip and chip-related stocks in other markets, for example ASML (Netherlands), SK Hynix and Samsung (South Korea), TSMC (Taiwan) and various niche semiconductor stocks in Japan. However, there was a pullback in the sector from late June, with many chip stocks giving up 20-25% from their highs. The semiconductor sector has historically been prone to boom and bust cycles, so are we just witnessing another one of these, or are we in a “supercycle”? A supercycle is best defined as a permanent upward shift in demand. The case for a structural shift is that chip demand has now become divorced from PC and smartphone sales. Computing capacity has become a basic infrastructure that will be needed long into the future. Supply is constrained and will remain so, given the length of time needed to build new semiconductor fabrication plants. in the short term at least, the data centre builders (i.e. the hyperscalers and others) are far more worried about falling behind in building enough computing capacity than about overspending. Their huge investments will therefore likely continue for the foreseeable future. As a result, some analysts believe the cycle has not peaked yet.

Is AI a bubble? Some (hopefully) common sense reflections

We touched on this question six months ago in the January market report, concluding that we do not face a re-run of the dotcom crash. Here, we offer a few further thoughts.

As a new technology, AI will clearly disrupt some businesses and markets, and some companies will emerge as winners, while others will be losers. The winners will see huge share price appreciation, even from current levels, while the reverse will be true for the losers. The market is currently trying to work out which of the many potential candidates will be the ultimate winners – but in spite of all the analyses and forecasts at present, ultimately no one really knows. Since markets always overshoot, this process will inevitably push the share prices of certain stocks up too high, and they will crash back to earth later. We can also be fairly certain that there is hype in some parts of the AI narrative – we just do not know exactly where. A pragmatic approach to these unknowable’s is not to come down on one side or another, but to take a “both and” approach. All of these can be true at the same time: AI is a transformational technology and there is hype in some parts of the narrative and there will be a bear market in equities at some point. This points (a recurrent theme of our market reports) to maintaining a diversified portfolio that is exposed to the opportunities, but also hedges some of the risks. A diversified portfolio is, by definition, one that takes a balanced view and does not concentrate on just one theme.

An important difference between the AI boom and previous bubbles, such as the dot-com and the subprime mortgage bubbles, is that the AI boom is not founded on borrowing and leverage (like the house price bubble) or on unproven businesses (like the dot-com bubble). Most AI investment is being carried out by the magnificent 7 tech companies, which also all happen to be among the 10 largest companies in the world. They are hugely profitable and are financing this investment almost purely from their own free cash flow. In a sense, the hyperscalers could stop investing tomorrow and their businesses would be largely unaffected. There would be a bust for some of their suppliers further down the value chain, but the tech giants themselves would sail on regardless.

Would an AI downturn drag the rest of the stock market down with it? There is a strong chance it would, but it is not certain. An optimistic reading of market movements over the past month is that some of the steam has already come out of the AI story and the slack has been taken up by other areas of the market, without equity markets falling in aggregate. The absence of leverage in funding the AI investment boom is important here. At the level of the public markets, there is no chance of a vicious and self-feeding cycle of market declines leading to rapid deleveraging, as occurred during the financial crisis. If publicly listed semiconductor stocks, or even tech stocks in general, were to halve, this would not jeopardise the survival of these businesses. Some corners of the market, such as private markets, where there is a higher degree of leverage, could experience turmoil, which could blow back on the banking system, but would be unlikely to pose an existential risk.

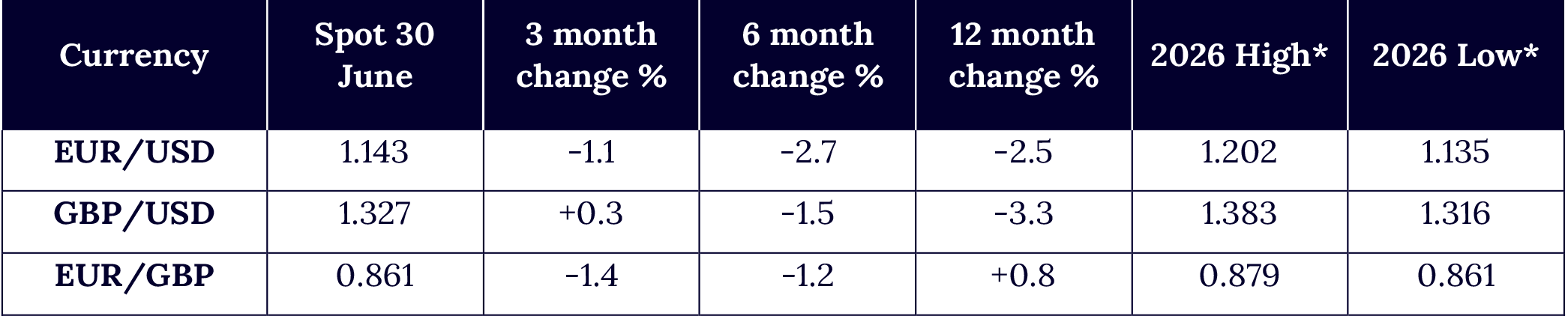

The following themes are intended as food for thought and do not represent a formal currency forecast.

Recent trend: down (stronger dollar)

Outlook: down

Recent trend: neutral

Outlook: neutral

Recent trend: down (stronger sterling)

Outlook: down

With the Iran war ‘over’ and oil prices retreating back to pre-war levels, we are moving back from a cautious stance to a neutral one. This means we expect the markets to be driven primarily by macroeconomic fundamentals and industry/business performance going forward. We believe investors should continue to embrace the opportunities that equity markets offer, while maintaining substantial positions in less risky assets such as bonds and cash in recognition of the heightened background risks.

Within equities, the AI theme is clearly important and there will be some big winners in this space who will see large share price gains. But diversifying beyond this theme in terms of geographies, industries and small and medium caps, or maintaining broad global exposure (which automatically provides some diversification), is advisable. Care needs to be taken in ensuring that a portfolio really is diversified, as interdependencies have increased. AI dominates not just some equity markets but is also a key driver of the macroeconomy (e.g. in the US), creating a double dependency. Some emerging markets, previously thought of as diversifiers, are even more concentrated AI bets than the US – Taiwan and South Korea, for example.

After several years of rapid gains, gold’s bull run came to a halt in the second quarter, as geopolitical risks faded and expectations grew of possible US rate hikes. Gold has become more volatile over the past year or two but still has a role to play as a hedge in portfolios.

Turning to the less risky assets, bonds have recovered after a sell-off at the start of the Iran war. Clearly, bonds would be hit by an increase in US interest rates. But if inflation eases in the US and elsewhere faster than expected, bonds could see a rally for the first time in many years. There is therefore potential upside, but the timing is uncertain at present. Given the uncertainties, an allocation to cash also makes sense in the current environment.

The outlook has improved, but the case for becoming significantly more bullish remains unconvincing. The immediate geopolitical threat has receded, economic growth is holding up and the AI investment cycle continues to support markets. At the same time, inflation remains a concern, valuations are high in parts of the market, and geopolitical risks have not disappeared.

The more interesting development is the broadening of investment opportunities. Investors are shifting away from the handful of stocks that dominated markets in recent years, while improving prospects in other sectors and regions are offering more places to find returns. In this environment, success may depend less on taking more risk and more on being selective about where that risk is taken.

We therefore remain neutral on the outlook, favouring a well-diversified portfolio with a moderate and geographically diversified exposure to all mainstream asset classes and selective exposure to markets and sectors where valuations and fundamentals still offer room for further gains.

As always, the appropriate balance between risk and reward will depend on each investor's personal circumstances. We therefore encourage clients to maintain regular dialogue with us and their investment manager to ensure their portfolios remain aligned with their long-term objectives.

CEO