After months of steady gains, the mood is shifting. The AI boom is still powering tech stocks, trade tensions have eased, and inflation is cooling — but cracks are starting to show.

Download PDF VersionThe market turmoil that followed Liberation Day in April receded further into the distance in the third quarter. Stock markets continued to rise globally, led by technology stocks in the US, as the AI boom showed no signs of abating.

After the expiry of the US tariff pause in July, several countries and regions (including two of the largest exporters, the EU and Japan) struck trade deals with the US, typically at tariff rates of around 15%.

In the last few quarters we described our outlook on the financial markets as "cautiously optimistic". This was based primarily on the market-friendly economic conditions, as the major economies are still unwinding the excesses of the post-Covid surge in inflation.

No major economy is in recession and inflation and interest rates are still trending down overall. We believed the Trump trade war would not be sufficient to derail this favourable backdrop, whatever the sound and fury surrounding it.

This quarter we are shifting our view to “neutral.”

While we continue to see the benign economic conditions as a strong card for the markets, we believe there are more potential downside risks.

In our view, the optimistic and pessimistic scenarios are now evenly balanced (see our “Reasons to be optimistic” and “Reasons to be cautious” below for further details).

The next few months will be pivotal in determining whether tariffs feed through significantly to US inflation, and how the Federal Reserve responds. The market is expecting a steady series of rate cuts and anything less would be a disappointment.

We will also get a read on whether the slowdown in the US labour market is spreading to other parts of the economy and causing a more general economic slowdown. And if the AI boom will continue, with capital spending and stock prices continuing to go in one direction only, or whether it will lose steam due to a reassessment of the business prospects of one of the main players, or the technology itself?

The 90-day suspension of US tariffs of over 100% on China expires in November. US-China trade talks are continuing behind the scenes and there have been hints of a possible meeting between Trump and Xi in November and a possible comprehensive deal. A deal would clearly be very positive for financial markets.

Job growth has slowed dramatically in the US, averaging just 30,000 per month between June and August, compared with 150-200,000 last year. However, there is debate about whether this reflects a genuine slowdown in the labour market or is predominantly a result of the fall in immigration and increase in deportations from President Trump's hardline immigration policy.

The unemployment rate is still low at 4.3% and has only ticked up marginally from its cyclical low of 4.1%. "Breakeven" job growth – i.e. the level that keeps the unemployment rate unchanged – has clearly fallen considerably, but Fed Chair Powell's estimate of around zero to 50,000 per month is no more than an educated guess. There is certainly a risk that weakness in the labour market could beget further weakness and feed through to consumer spending and other areas of the economy.

The current government shutdown could also hit the job market if President Trump carries through on his threat to permanently fire, rather than furlough, government employees.

Manufacturing remains one of the softest parts of the economy. With the exception of two months at the start of 2025, the Institute for Supply Management (ISM) index has been below the expansion/contraction threshold of 50 for around three years. It stood at 49.1 in September. Consumer spending has held up relatively well, however, with retail sales growing at around 4% yoy in recent months (around 1% in real terms), although consumer confidence has been persistently weak.

Gross domestic product (GDP) grew by 3.8% in Q2 following a 0.6% fall in Q1. Averaging the two quarters gives a growth rate of 1.6% - sluggish but nowhere near a recession. This is below-potential growth, which should put downward pressure on underlying inflation and is probably one of the reasons why the feedthrough of tariffs to inflation has been relatively limited so far.

Consumer Price Index (CPI) inflation has moved up from a low of 2.3% in April to 2.9% in August, though core CPI excluding food and energy costs only increased from 2.8% to 3.1% over the same period. Personal Consumption Expenditures (PCE) inflation, the Fed's preferred measure, has similarly ticked up from 2.6% to 2.9%. However, some analysts fear the worst of the tariff impact may be yet to come through, as importers have either been running down stockpiles or absorbing much of the cost until now.

While inflation has gone up by less than feared as a result of tariffs, it has still been moving in the wrong direction, away from the Fed's target. As the Fed has acknowledged, this has created a conflict between the two parts of its mandate.

The Nasdaq continued its rebound after the slump earlier in the year, advancing by 11% in the third quarter. Technology stocks were helped by the absence of much tariff-driven inflation and the 25bp Fed rate cut in September. The economic growth slowdown is probably also positive for technology stocks, at least in relative terms, as their businesses are less affected by the economic cycle.

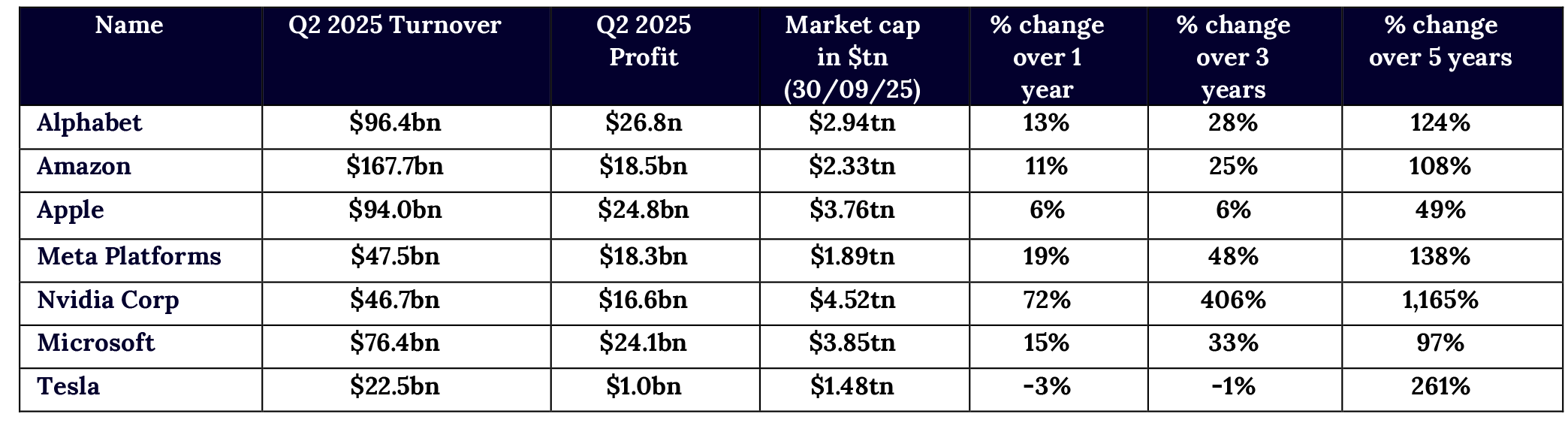

Within the Magnificent 7 (Mag 7), the stocks that lagged in the first half of the year were strongest in the third quarter. Performance was led by Alphabet, Apple and Tesla, Microsoft eked out a small gain and Amazon and Meta were roughly flat, with Nvidia in the middle of the pack. Year-to-date Nvidia still leads the way with a price gain of 28%, followed by Alphabet, Meta and Microsoft at around 20% each.

Amazon, Apple and Tesla lag well behind – flat in Amazon’s case and just a 1% gain for Apple.

Tesla's performance is distorted by the enormous run-up after the presidential election and comedown in early 2026. It is the best-performing Mag 7 stock over the past year, with a rise of 70%.

There have been some signs of a modest pickup in the eurozone economy this year. GDP growth was 1.4% in the first half of the year, more or less in line with the US. Purchasing managers’ indices have recovered over the course of the year to 49.5 for manufacturing and 51.4 for services in September, indicating that the manufacturing recession has ended. With the tariff shock digested by now, this is a hopeful sign that the euro area economy can pick up from here.

There are indications that the German economy, which has been the euro area's problem child over the last few years, is steadying. The ifo business climate index, a reliable leading indicator of the German economy for decades, has trended up over the course of the year, though it fell back unexpectedly in September. Germany's expansionary fiscal policy is forecast to boost growth significantly in 2026 and 2027.

Where Europe differs most markedly from much of the rest of the world is that inflation is now more or less back on target. Following three consecutive months at 2.0%, euro area CPI inflation ticked up to 2.2% in September, with core inflation at 2.4%. This has allowed the European Central Bank (ECB) to cut its policy rate to 2%, which should boost the European economy.

UK GDP grew by 0.3% quarter-on-quarter in Q2, after 0.7% in Q1, a very similar performance to the US and the euro area.

Retail sales were roughly flat in real terms in the three months to August and are still 2% below the pre-pandemic level of February 2020. The labour market has cooled a little, with the unemployment rate rising from 4.2% to 4.7% over the past year. Perhaps unsurprisingly, since overall economic growth is broadly similar, purchasing managers' indices are at comparable levels to the US and eurozone, with the S&P manufacturing PMI in modestly contractionary territory at 47.0 in September and the services PMI at 51.9, showing modest growth.

The UK's main economic challenge is its stubbornly high inflation. Consumer Price Index (CPI) inflation was 3.8% in August, with services inflation of 4.7% and wage growth of 4.8%. This has forced the Bank of England to move slowly in lowering interest rates.

The relative boost to the UK economy from the limited trade deal with the US is likely to be small. It has secured a slightly lower tariff rate of 10% on a fixed quota of car exports and 25% on steel and aluminium (instead of 50%). Moreover, it is out of the firing line in any future trade spats, which would help if a full-on trade war erupted, which certainly cannot be ruled out.

The Japanese economy grew 2.2% annualised in Q2, after 0.3% in Q1. Overall, this is the same moderate pace of growth of around 1-2% as in other major economies. The widely-watched Tankan business confidence index of large manufacturers is similarly steady, fluctuating between a net positive score of 12 and 14 over the last 18 months.

The uncertainty surrounding trade has been removed by the trade deal with the US giving Japan a 15% tariff rate on most goods exports. Japan's core inflation is well above the Bank of Japan's target at 3.3% in August and expectations of another rate hike in October are growing.

The change of leadership following the resignation of Prime Minister Ishiba in September could herald a shift in economic policy. The current frontrunner in the ruling LDP party's leadership election set for October, Sanae Takaichi, favours a more aggressive pro-growth policy in the mould of Shinzo Abe. She would probably increase fiscal deficits and has questioned the need for the Bank of Japan to raise interest rates. This policy mix could boost growth and lead the yen to weaken further.

The Fed cut interest rates by 25bp in September to the target range 4.0% – 4.25%, justifying the cut by a shift in the balance of risks, as reflected in the slight rise in the unemployment rate. The market is expecting a series of rate cuts amounting to around 1% over the next year. But Chair Powell struck a cautious note after announcing the rate reduction in September, stating that the Fed would need to continue balancing the opposing risks of above-target inflation and the slowdown in the labour market. The "dot plot" of the Federal Open Market Committee’s (FOMC) interest rate forecasts is similarly split, with the forecasts for rates at the end of 2026 ranging from 2.4% to 3.9%.

President Trump has kept the Fed under intense political pressure, calling for interest rates to be slashed to 1% and accusing Powell of being too slow and too late to act. It will be difficult for the Fed to resist this pressure to ease monetary policy further. The president has already placed one supporter, Stephen Miran, on the FOMC and attempted to remove another committee member, Lisa Cook, for alleged fraud, but the Supreme Court has stayed her removal until at least January. Whether Trump succeeds in removing Cook or not, he will nominate a new Fed chairman to replace Jerome Powell, whose term ends in May 2026, early next year. The only question is how dovish a figure he will nominate, and whether it will be a mainstream economist or a more fringe figure. Either way, the US looks set to have much easier monetary policy over the next 18 months.

Having halved interest rates from 4% to 2%, making it the fastest to cut rates in the developed economies, the ECB stayed on hold in the second quarter. It now sees the risks to growth and inflation as more evenly balanced.

The Bank of England trimmed interest rates by 25bp to 4.0%. It continues to express concern at the relatively elevated level of inflation, although it has acknowledged some progress in easing wage pressures. These constraints are expected to ease eventually and allow the Bank of England to cut rates further later this year and into 2026.

In spite of well above-target inflation, the Bank of Japan (BoJ) left its policy rate unchanged at 0.5% in the third quarter. It argues that inflation has been pushed up mostly by temporary factors and inflation expectations are not yet anchored at 2%. However, the trade deal with the US has removed an important impediment to a possible rate hike. A 25bp rate hike to 0.75% is therefore widely expected at the next monetary policy meeting at the end of October.

Our more neutral view this quarter implies a more cautious asset allocation, but it is important not to overdo the pessimism.

We still see opportunities in equity markets. The US stock markets have continued to perform well this year but are no longer leaving other stock markets trailing so far behind. The US, UK, Europe and Japan have all performed roughly in line with each other in 2025.

Emerging markets have had a much stronger year, benefiting from the weaker dollar and the fall in US interest rates and have outperformed the developed markets overall.

Gold has remained a star performer, with the gold price rising around 18% in the third quarter and approaching the $4,000 level. Over the past year the gold price is up over 40%, well ahead even of the Nasdaq index. This reflects a cocktail of concerns about geopolitics, inflation, debt levels, the US government shutdown and attacks on central bank independence, to name just a few (the list could go on), as well as economic and structural factors such as diversification of central bank reserves and falling US interest rates.

Government bond yields have effectively been moving sideways for two years since their sharp rise in 2022 and 2023. Debt worries, fears of a tariff impact on inflation and stubborn inflation generally are being counterbalanced by the continuing fall in short-term interest rates.

Corporate bonds, particularly high yield, have continued to perform well owing to the benign credit conditions resulting from steady economic growth. With bond yields still relatively high (compared with the 2008-2022 period), bonds offer an attractive risk-reward profile. Bonds would rally in most of the pessimistic scenarios we have highlighted (in particular, a downturn in the US economy), and could even rally in a more optimistic scenario, unless inflation rises significantly, which is only an outside risk.

Stock markets have had another good year. We are now neutral between optimistic and pessimistic views of the future, which implies pegging back risk a little.

It is more important than ever to maintain a well-diversified portfolio, maintaining a moderate and diversified exposure to all mainstream asset classes – equities, bonds, gold and cash – depending on each individual's situation.

Constant dialogue with your investment manager is key to understanding your personal risk/reward profile, and we are here to help guide that process.

CEO