The year did not begin as expected. Conflict, rising energy prices and a shift in inflation dynamics have changed the backdrop for markets, and with it, the balance of risks.

Download PDF VersionFor several years, the global economy has defied repeated predictions of recession, despite higher interest rates and the introduction of tariffs. This resilience has supported equity markets over the past three years.

The recent surge in energy prices, driven by the Iran conflict, now presents a more meaningful test. While the impact may prove less severe than feared, current indications suggest it could prove more pronounced than previous shocks.

Unlike in 2022, there is less support from government spending and household balance sheets are not as strong. As a result, higher energy prices may weigh more heavily on growth, even if the inflationary impact is less extreme. A resolution to the conflict is also unlikely to deliver an immediate normalisation in prices or supply.

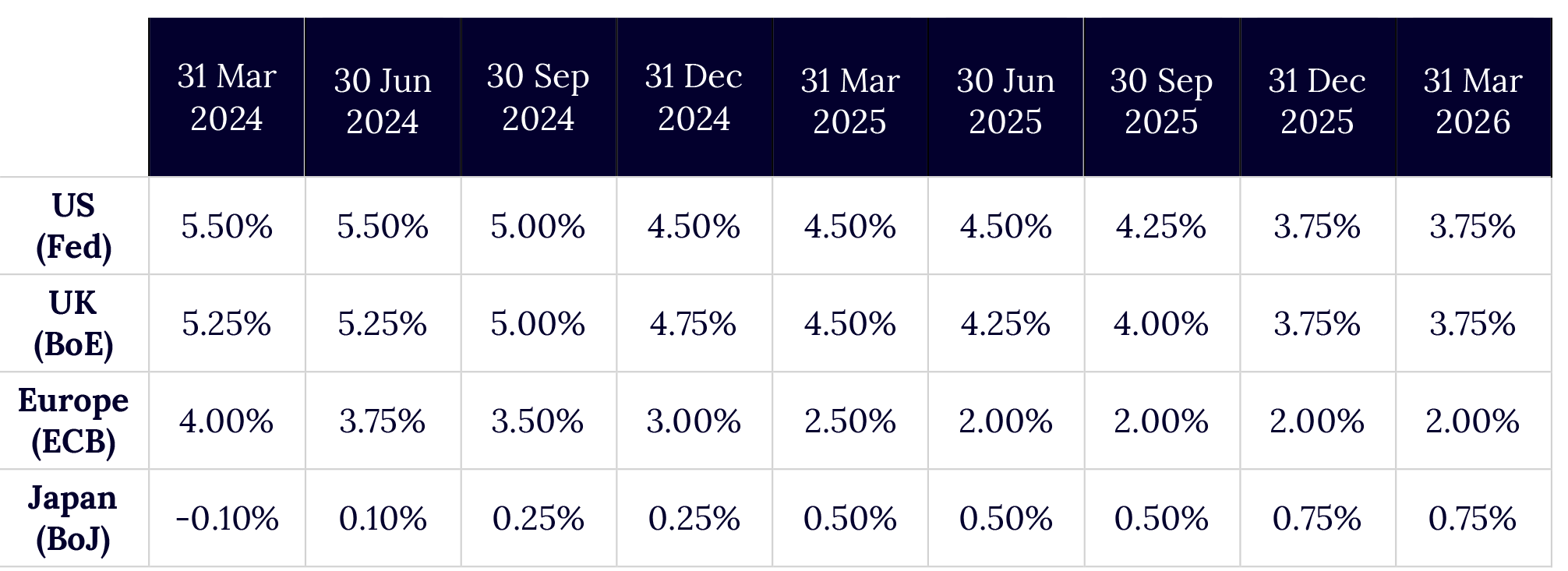

We identified rising US inflation as a key risk at the start of the year, and this is now beginning to materialise. Markets have responded accordingly, with pressure across equities, bonds and gold, while cash has held up relatively well.

A more favourable outcome would involve a quicker resolution, easing energy prices and a gradual return to rate cuts. However, this may take time. For now, central banks remain in a holding pattern.

Given continued volatility and uncertainty, including the risk of further escalation, we have moved our outlook from neutral to cautious.

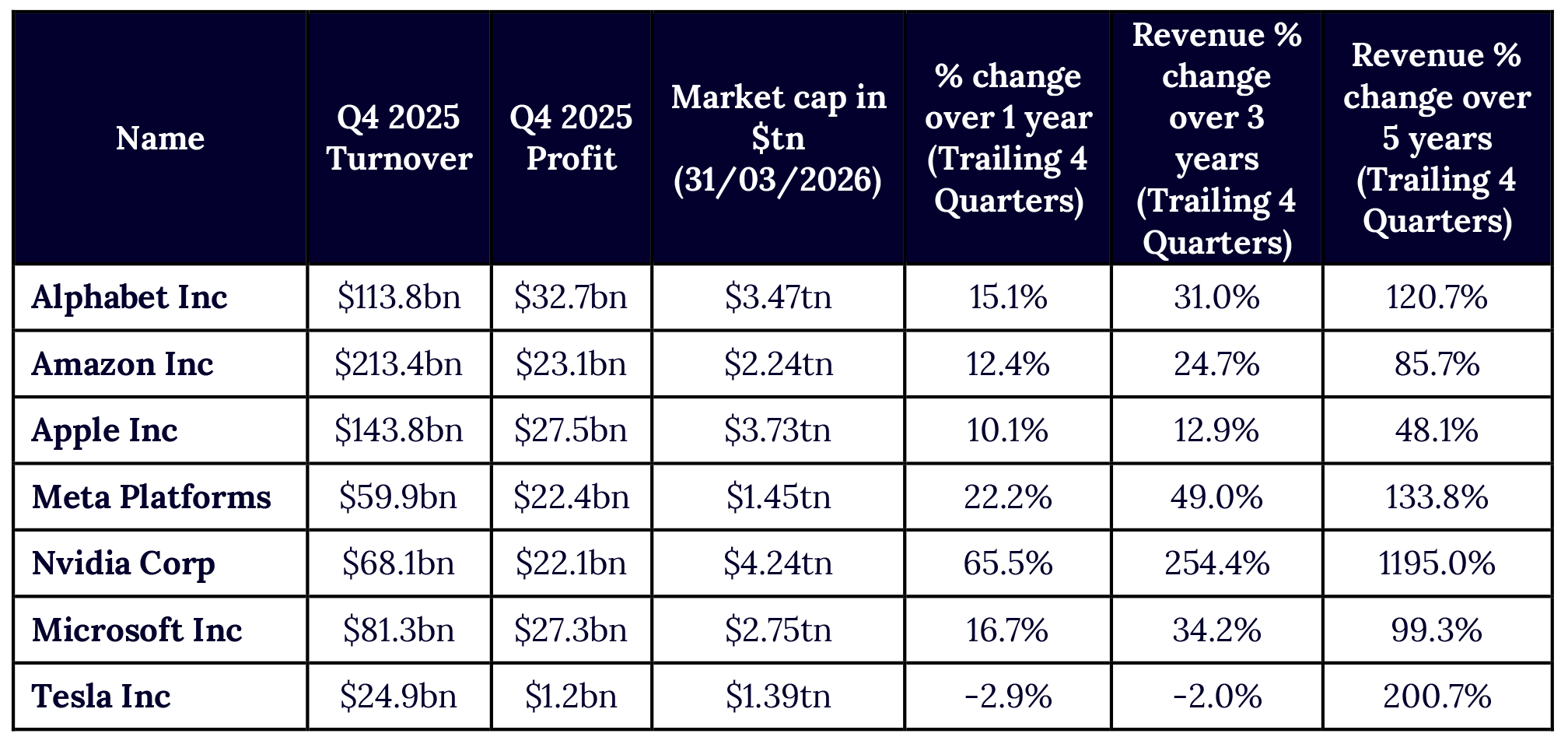

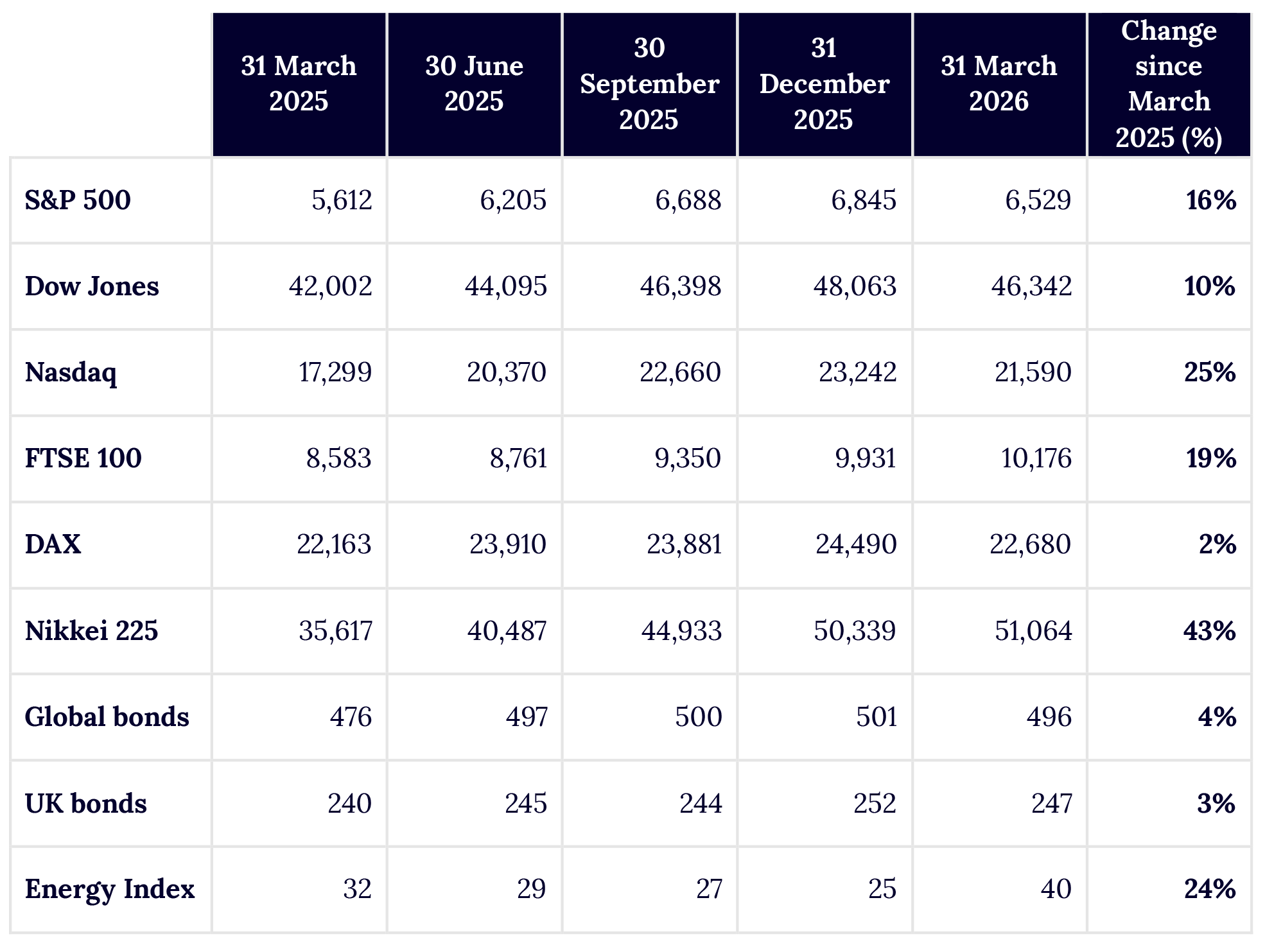

Technology stocks fell sharply in the first quarter, with the Nasdaq down 7% and most of the Magnificent 7 underperforming, led by a near 25% decline in Microsoft. Unlike last year’s recovery after a weak start, a similar rebound in 2026 appears less certain. The sharpest falls were in software and services, where AI is expected to disrupt existing business models.

As a growth sector, technology is sensitive to rising inflation and interest rate expectations. However, the recent weakness also reflects growing scepticism around the scale and returns of AI-related capital expenditure. These investments are absorbing significant free cash flow and challenge the sector’s traditionally asset-light model, with long-term profitability still uncertain.

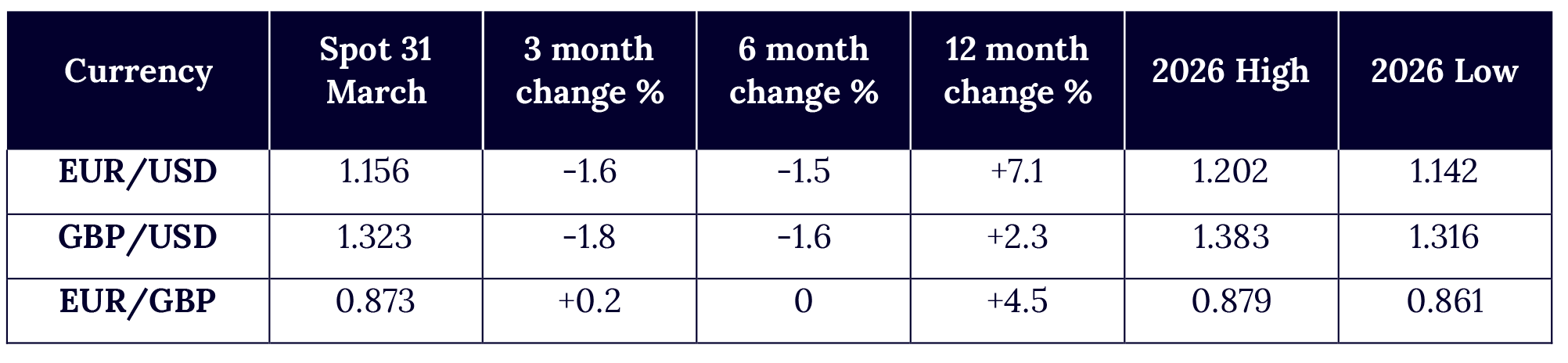

Recent trend: slightly down (stronger dollar)

Outlook: ambiguous

Recent trend: slightly down (stronger dollar)

Outlook: ambiguous

Recent trend: neutral

Outlook: neutral to up (stronger euro)

This quarter, we have moved from a “neutral” to a “cautious” outlook on the financial markets, as we believe the downside risks have increased. Of course, there is still upside potential in riskier asset classes such as equities and there are still possible positive scenarios for the future (particularly in the medium term), even though we believe these are less likely at present. As before, we recommend holding a moderate allocation in all mainstream asset classes. A moderate, diversified allocation would have weathered the market downturn since February reasonably well.

Gold’s bull run was finally interrupted in the first quarter as it reached a record high of $5,300 before retreating. It was still up 8% in the first quarter as a whole, however, and 60% over the past year. It is hard to see gold exceeding this peak, so for now upside may be limited. Gold has become riskier and more volatile over the past year or two but still has a role to play as a hedge in portfolios.

As we noted last quarter, bonds are in some ways the linchpin asset class in 2026. Predictably, bonds were hit in the initial energy price spike, as inflation fears took hold and the market switched from anticipating rate cuts to building in forecasts of rate hikes. But if the inflation spike leads to an economic slowdown, bonds could eventually rally. If bonds continue to struggle, we could face a 2022 scenario where all asset classes except cash perform badly.

In practice, this reinforces the importance of maintaining alignment between portfolio structure and long-term objectives, rather than reacting to short-term developments.

The outlook remains uncertain, particularly in relation to inflation and the potential impact of higher energy prices on growth. While the direction is not yet clear, this reinforces the need for a measured and disciplined approach.

In this environment, well-structured and diversified portfolios should be designed to absorb periods of volatility without requiring reactive change. Our focus remains on ensuring each portfolio continues to reflect long-term objectives, risk tolerance and liquidity needs, supported by ongoing dialogue and careful review.